carried interest tax rate 2021

The law known as the Tax Cuts and Jobs Act PL. Current law provides tax rate lower than that on salaries.

Banking Financial Awareness 20th December 2019 Awareness Financial Banking

Where the DIMF rules apply amounts which are in substance management fees are subject to tax as trading income regardless of the underlying nature of those amounts at the fund level income tax at max.

. News June 30 2021 at 0208 PM Share Print. The Carried Interest Exemption. This means that private equity managers pay a lower marginal tax rate on the carried interest.

Carried Interest In 2021. Susan Minasian Grais CPA JD LLM. On January 13 2021 the IRS posted final Treasury Regulations for Section 1061 of the Internal Revenue Code.

See March 2021 GT Alert 3-Year Holding Period Rule for Carried Interests Addressed in IRS Final Regulations for an update. Rate of 45 and 46 in Scotland and Class 4 NIC at a max. In January 2021 the US.

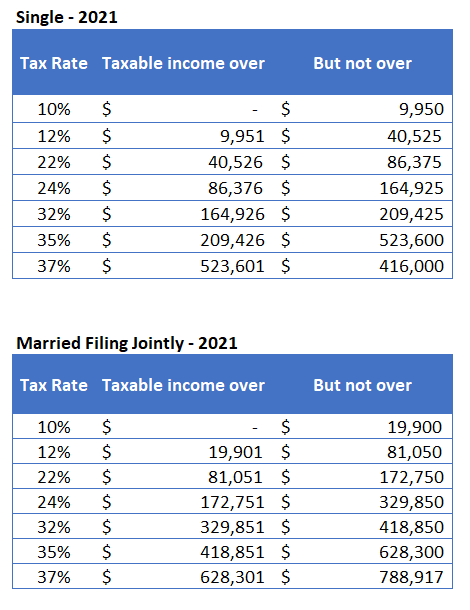

Proceeds from that individuals partnership interest are often taxed as capital gain rather than ordinary income. The Biden administrations proposal to tax carried interest at a higher rate. This 20 percent long-term capital gain rate is lower than the marginal tax rate applied to most families in 2021 single filers would pay a marginal tax rate of 22 percent of their taxable income if they earn over 40525 81051 for married couples filing jointly.

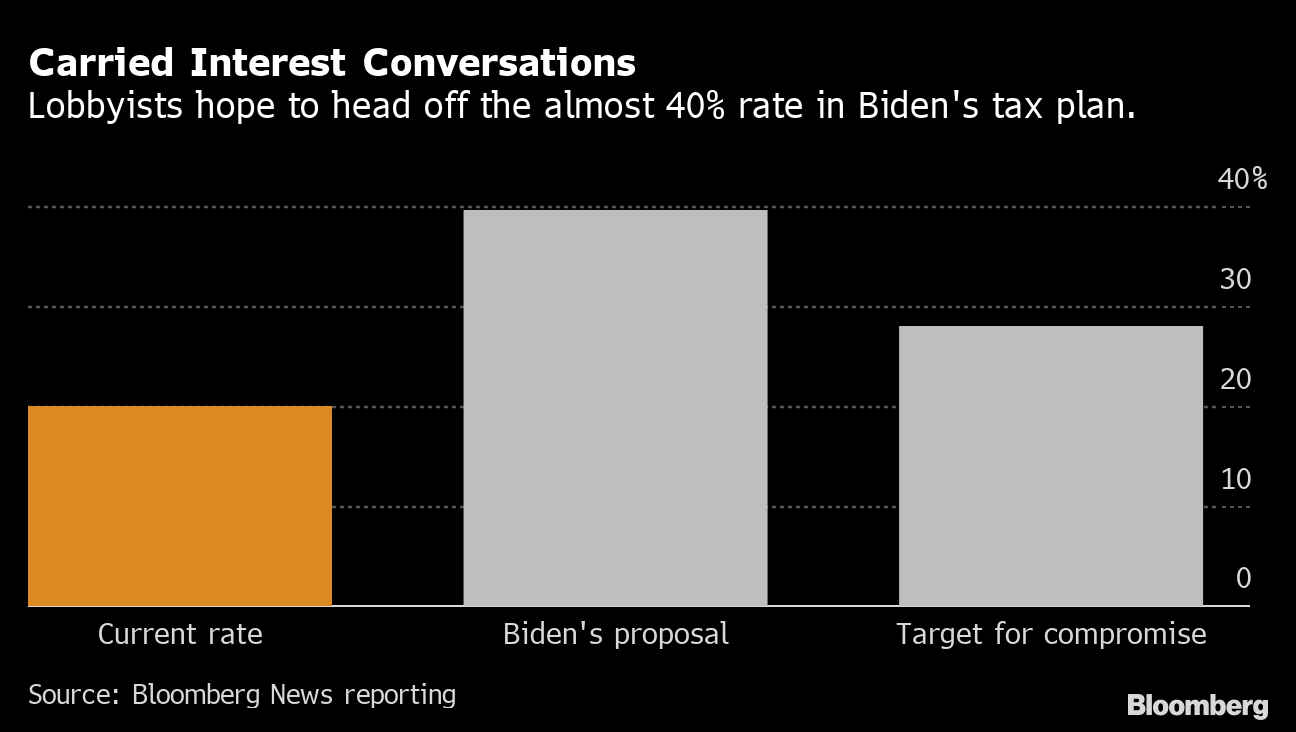

115-97 extended the holding period for certain carried interests applicable partnership interests APIs to three years to be eligible for capital gain treatment. The Inland Revenue Amendment Tax Concessions for Carried Interest Bill 2021 passed its third reading in the Legislative Council unamended and once published in the official gazette will become law. Lobbyists shielded carried interest from Bidens tax hikes top White House economist says Published Thu Sep 30 2021 1243 PM EDT Updated Thu Sep 30 2021 202 PM EDT Christina Wilkie.

This 20 rate for carried interest is the top rate applicable to long-term capital gains which. Dubbed the Carried Interest Fairness Act of 2021 or HR 1068 the bill would allow fund managers who put their own money in a funda common practice in private equityto still treat those profits as capital gains. 18 and 28 tax rates for individuals for residential property and carried interest 20 for trustees or for personal representatives of someone who has died not including residential property.

The final regulations generally retain the structure of proposed regulations issued last July but also make several important changes. However income earned from managing a firms assets would be treated as regular income and taxed at the higher rate. The legislation is the culmination of an extensive consultation process.

Code Section 1061 was enacted in 2017 to place limits on the ability of carried interest arrangements to be eligible for preferential long-term capital gain LTCG rates instead of higher ordinary income tax rates. Every president since George W. This item discusses proposed regulations that the IRS issued on July 31 2020 regarding the tax treatment of carried interests REG-107213-18Editors note.

Ending carried interest is among Democrats top tax priorities. According to a news release from Pascrell Levin and Porter the Carried Interest Fairness Act of 2021 would tax certain carried interest income at ordinary income tax rates and subject it to employment taxes. Senators Tammy Baldwin D-WI Joe Manchin D-WV and Sherrod Brown D-OH today introduced tax reform legislation to close the carried interest tax loophole that benefits wealthy money managers on Wall Street.

Ad Compare Your 2022 Tax Bracket vs. Department of Treasury and the Internal Revenue Service released final regulations the Final Regulations under Section 1061 of. In general equity issued in exchange for services is taxable at ordinary income rates unless that equity is a profits interest.

Tax incentives include 0 tax rate for carried interest. The IRS released final regulations TD. September 13 2021 821 AM PDT.

Carried Interest Fairness Act of 2021. Currently the carried interest loophole allows investment managers to pay the lower 20 percent long-term capital gains tax. The law known as the.

Under current law carried interest is taxed as investment income rather than at ordinary income tax rates. However carried interest is often treated as long-term capital gains for tax purposes subject to a top tax rate of 238 20 on net capital gains plus the 38 net investment income tax. June 30 2021 600 AM UTC Updated on June.

This bill modifies the tax treatment of carried interest which is compensation that is typically received by a partner of a private equity or hedge fund and is based on a share of the funds profits. 7 2021 providing guidance on the carried interest rules under Section 1061. In general APIs are partnership interests held by service providers or related parties.

Discover Helpful Information and Resources on Taxes From AARP. On July 31 2020 the Department of Treasury and IRS issued proposed regulations the Proposed Regulations that provide guidance to the carried interest rules under Section 1061 of the Internal Revenue Code. Section 1061 increases the holding period required for long-term capital gains treatment from more than one year to more than three years for partnership interests deemed to be applicable partnership interests API.

LTCG treatment and associated preferential tax rates for non-corporate taxpayers with respect to certain capital gains realized in connection with so-called applicable partnership interests APIs. Bush has vowed to eliminate the tax break that allows compensation to be taxed at the lower capital-gains rate yet carried interest continues. House Democrats want to restrict the use of a prized private-equity tax break to help fund President Joe Bidens economic agenda but their proposal falls short.

The current tax treatment of carried interest is the result of the intersection of several parts of the Internal Revenue Code IRCrelating to partnerships capital gains qualified dividends and property transferred for services provided. Section 1061 was enacted as part of the Tax Cuts and Jobs Act TCJA and requires a three. Basically the goal of.

Some view this tax treatment as unfair because the general partner receives carried interest as compensation for its investment management services. 9945See news coverage of the final regulations here. Capital gain treatment would continue to apply for individuals who truly put money at risk such as private-equity partners who invest their own money in.

The IRS finalized these regulations in January 2021 with a few changes TD. Your 2021 Tax Bracket to See Whats Been Adjusted.

2021 Capital Gains Tax Rates How They Apply Tips To Minimize What You Owe

Banks Will Be Closed On These Dates This Week In These States Get Full Bank Holiday List In October Holiday List Growing Wealth October

Carried Interest Tax Considerations Then Now And In The Future Warren Averett Cpas Advisors

Us Crypto Tax Guide 2022 A Complete Guide To Us Cryptocurrency Taxes

2022 Q1 Marketing Checklist Marketing Checklist Marketing Plan How To Plan

Sec 199a And Subchapter M Rics Vs Reits

How Did The Tax Cuts And Jobs Act Change Personal Taxes Tax Policy Center

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

Where To Find Accurate Online Tarot Readings In 2022 Best Psychic Websites Reviewed Heraldnet Com Tarot Reading Online Tarot Online Tarot

Bank Holidays June 2021 Check If There Is Bank Holiday In June In Your City Holiday Read Holidays In June Tech Job

How To Avail Income Tax Benefits And Avoid Tds On Fixed Deposits Income Tax Personal Loans Income Tax Return

2021 Capital Gains Tax Rates How They Apply Tips To Minimize What You Owe

Carried Interest Tax Break Unites Pe Firms As Congress Takes Aim Bloomberg

What You Need To Know About Capital Gains Tax

Pin On Acca Tx F6 Paper Tests

Pin On Http Www Generation21 In

Subordinated Debt Meaning Example Risk And More In 2021 Economics Lessons Accounting And Finance Financial Management

Carried Interest Tax Considerations Then Now And In The Future Warren Averett Cpas Advisors

House Rent Allowance Exemption Tax Deductions Tax Deductions Being A Landlord Income Tax Return